That first six-figure sum hits different.

It’s not the delirious joy you see in financial influencer clips. It’s a quiet Ah moment on a Tuesday evening, staring at your Depot screen, followed immediately by the cold splash of reality. Because in Germany, a six-figure portfolio isn’t just a number, it’s a battlefield where your future self and your present self are in a constant tug-of-war.

One wants a funded retirement, preferably sipping Apfelschorle on a Balkon overlooking Tegernsee. The other wants a funded Eigenkapital deposit for an Eigenheim (home) so you can stop experiencing the annual Berlin rental market panic attack. I recently came across the story of a German engineer who, at 26, hit this precise milestone. With a net income of €3,500, he saves a staggering €2,400 a month. His secret weapon? Living in his partner’s parents’ basement for a “fair contribution” to costs, keeping his total monthly expenses under €1,000.

But here’s the wrench in the Sparplan (savings plan): a house. He’s managing two separate portfolios: one for his Altersvorsorge (retirement), and a separate liquid one, investing in something like the LYX0WM (a money market ETF), earmarked for an imminent Hausbau (home construction). His goal? Have €100k parked for the future before he touches any of it for the home loan.

This isn’t just saving, this is high-wire asset allocation. And it’s the most German financial conundrum you can face. Let’s unpack how to dance this delicate tango without falling flat on your face.

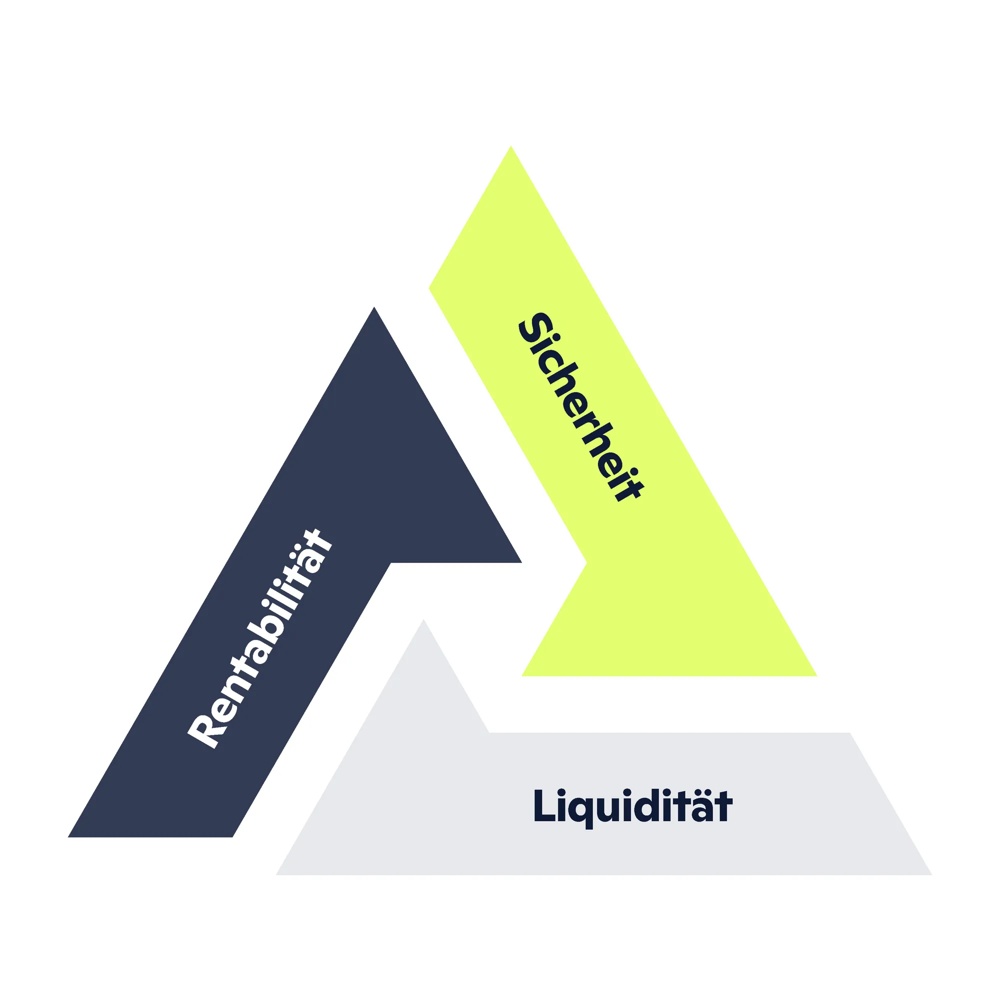

The German Financial Triangle: You Can Only Pick Two

All investing wisdom gets filtered through a pragmatic, German-engineered lens here. Forget high-risk, high-reward gambles for a moment. Old-school German financial planning operates on a principle so fundamental it’s often diagrammed as a triangle: Sicherheit (Security), Rentabilität (Profitability), and Liquidität (Liquidity). The rule? You can only ever maximize two at the expense of the third.

Want high security and high liquidity? That’s your Tagesgeldkonto (savings account). Enjoy your ~1.8% annual return. Want high security and high profitability over time? That’s a locked-in, long-term Bausparvertrag (building savings contract) or retirement portfolio. But you can’t touch it. Want high profitability and liquidity? Hello, volatile stock market. Your money’s there, but its value on any given Tuesday is a mystery.

This triangle explains why our engineer friend has two Depots. The long-term Altersvorsorge is for Sicherheit and Rentabilität. The LYX0WM pot is for Sicherheit and Liquidität, it needs to be stable and accessible when the builder calls for the next invoice.

The Liquidity Labyrinth: Notgroschen vs. Eigenkapital

In English, you have an “emergency fund.” In Germany, you have a Notgroschen, which literally means “emergency penny.” It’s money you can access instantly, without selling assets at a bad time.

But what about money earmarked for a major life goal that’s 2-5 years away? That is your tactical liquidity pool. The problem is, most Germans park this in Tagesgeldkonten (savings accounts), chasing promotional rates from bank to bank. It’s a mental drain.

Enter the Geldmarkt ETF (money market ETF), like our friend’s LYX0WM. These funds invest in ultra-short-term, highly secure debt (like overnight loans between banks) and aim to mirror rates like the €STR (Euro Short-Term Rate).

In 2026, while your local Sparkasse might be paying 1.5% on a Tagesgeld bestandskunde rate, a Geldmarkt ETF can track the €STR at, say, 2.0% minus a tiny fee (0.05-0.15%). The catch? It’s not instantly transferable and is only tradeable during Börsenzeiten (market hours), settling in T+2 days.

This is the modern compromise for the financially organized: your tactical Eigenkapital pot isn’t losing value to inflation by much, and it lives right inside your main investment depot, reducing mental clutter. As one analysis put it, having a Notgroschen auf dem Depot parken is the organized way to manage liquidity.

The Coming Revolution: Your ETF-Sparplan Gets a State Sponsor

Now, let’s complicate this beautifully. The German government’s reform of the Riester system is bringing the Altersvorsorgedepot (pension investment account) starting in 2027. This will be a state-certified, private-depot wrapper where your own ETF investments can attract government bonuses and tax advantages.

But, crucially, it’s a walled garden. You can’t just convert your existing Depot. You need a new, state-certified one, and you can only buy government-approved assets (ETFs in risk classes 1-5). Want to scale your monthly ETF contributions? This could be a new, tax-advantaged path. Maximum contributions will be capped (likely €6,840 annually), and early withdrawal for anything other than wohnwirtschaftliche Zwecke (property purchase, construction, or renovation) means paying back all those sweet state subsidies. But buying a house? That’s an approved escape hatch.

This creates a future scenario where savvy savers will have three pots: a flexible Geldmarkt ETF for down-payment liquidity, an Altersvorsorgedepot for the tax-efficient, state-subsidized core of their retirement, and a standard, unrestricted Depot for everything else. The German financial life is becoming a game of jurisdictional chess.

So, How Do You Actually Allocate?

The theory is clear. The practice is personal. Based on countless discussions and the philosophy behind automating salary routing for savings growth, your strategy might look like this:

- Define Your Time Horizons. The Anlagehorizont (investment horizon) is everything. Money needed in <3 years (house deposit)? Sicherheit & Liquidität rule. Geldmarkt ETF or a ladder of Festgeld (term deposits). Money for 10+ years (retirement core)? That’s your Rentabilität & Sicherheit zone. All-in on a globally diversified ETF-Sparplan, likely housed in the coming Altersvorsorgedepot. A chunk for 3-10 years (maybe a child’s education or a sabbatical fund)? This is your hybrid zone. A conservative mix of assets, maybe a Rentenfonds (bond fund) or solid dividend ETFs.

- Prioritize Tax Shelters. Always max out tax-advantaged space first. If you’re eligible for an Altersvorsorgedepot, use it. Before you invest in a standard brokerage account, ensure your employer’s bAV (betriebliche Altersvorsorge, company pension) and the new state-sponsored plans are optimized. This is a key principle for those exploring strategies for starting wealth later in life.

- Embrace the Two-Depot System. Like our engineer, mentally and logistically separate your long-term, “don’t-touch” wealth from your life-goal liquidity. It removes the emotional friction of “dipping into” your retirement fund for a new kitchen. The Altersvorsorge is for future you. The other pot is for present you.

The journey to your first €100k in Germany is less about raw saving power and more about adroit allocation. It’s understanding that German finance is a system of boxes: retirement boxes, house boxes, emergency boxes, each with different locks and keys. Your skill isn’t just filling them, it’s knowing which key opens which box, and when.

The goal isn’t just to amass capital. It’s to build capital that serves your actual life, a life that includes both a secure 65th birthday and a set of house keys long before that.