Your Family Isn’t Ready for Your Death: Navigating Germany’s Inheritance Minefield

Picture a scene repeated, in various shades of absurdity, across German living rooms, lawyer’s offices, and court corridors. The body of a grandparent isn’t even cold before close family are already “spontaneously” visiting, with lawyers in tow, to “check on” properties and bank accounts. Panic sets in. Half the family is convinced they’re getting screwed, the other half has already started screwing them by dipping into accounts “to keep the house build going.” No one knows if there’s a Testament (will), who’s in it, or how anything is supposed to be divided. Trauer (grieving) is replaced with Goldgräberstimmung (gold-rush fever).

The Post-It Note Estate Plan: Why Good Intentions Aren’t Good Enough

You might think your family is different. You trust them. Maybe you’ve even had a vague chat over coffee about “who gets Oma’s piano.” That’s not a plan, that’s a hopeful wish.

The horrific scenarios that play out often stem from two critical, preventable failures: the absence of a clear, legally-binding Testament (will) and a complete lack of communication about the gesetzliche Erbfolge (statutory order of succession).

Did You Know?

Explore more on the wealth gap between earned income and inheritance, which often fuels these tensions.

German law dictates who inherits if you die without a will. For a married couple with children, it’s a split between the spouse and kids. Sounds simple? It’s a recipe for an Erbengemeinschaft (community of heirs), a legal construct where all heirs own everything together. Want to sell the family home? Every single heir must agree. One stubborn sibling can block everything for years. This isn’t just a financial gridlock, it’ll tear your family apart.

Your handwritten, heartfelt letter is worthless if it’s not formalised. As legal experts emphasize, a notarielles Testament (notarial will) offers additional security and can prevent inheritance disputes. It’s witnessed, registered, and nearly impossible to challenge on a technicality. The cost, which scales with estate value, is a pittance compared to the six-figure legal war it can prevent.

The “Vorgezogene Erbe” (Early Inheritance) Trap: Goodwill Gone Wrong

A major trend, as noted in financial circles, is the rise of the vorgezogene Erbe (early inheritance). Parents, wanting to help their kids buy property or settle into life, transfer assets early. On paper, it’s generous. In practice, it’s a minefield.

Consider the all-too-common scenario: money is “gifted” for a house build. Years later, after the parent’s death, siblings who didn’t get such advances feel short-changed. Was it a gift or an advance on the inheritance? Was it documented? The resulting resentment poisons family gatherings forever.

This points to a crucial rule: Transparency is non-negotiable. If you give one child money for a house, document it clearly, ideally in the presence of a Notar (notary), and explain to all siblings how it will be accounted for in the final estate division.

When the Finanzamt (Tax Office) Becomes Your Least Worry

For the family home to be transferred tax-free to a spouse or child, strict conditions apply, as highlighted in German financial reporting. The inheritor must use the property as their primary residence for ten years. Not a weekend getaway. Not a rental property. Their main home. And they must move in within six months.

Imagine inheriting a home in a city where you don’t work. You’re forced to sell your current place, change jobs, or commute four hours a day. Fail to meet these conditions, and the Finanzamt claws back the tax exemption retroactively. “Dann verwirkt man das Steuerprivileg rückwirkend”, as tax lawyers warn.

And for children, there’s a kicker: the exemption only covers up to 200 square meters of living space. Anything larger gets taxed proportionally. Suddenly, that roomy Familienvilla (family villa) isn’t just an asset, it’s a looming tax bill.

The Nuclear Option

What happens if siblings inherit a property together? You’re back in the Erbengemeinschaft nightmare. One wants to sell, another to live in it, a third wants to rent it out. Deadlock. The nuclear option is a Teilungsversteigerung (partition auction), a court-ordered sale that often yields below-market prices and leaves everyone feeling violated.

Before you think “they’d never do that”, remember: money reveals character, and grief strips away pretense. The emotional value of a home is incalculable, making rational compromises nearly impossible.

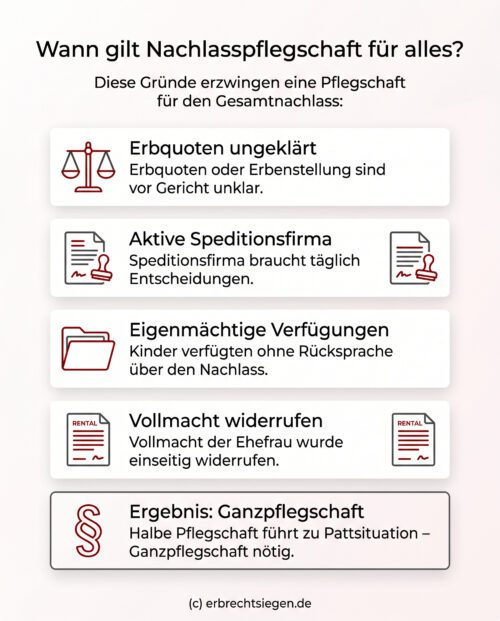

The Atomic Option: When the Court Takes Control

When heirs are at war, and assets are being pilfered or hidden, the situation may call for a legal Nachlasspflegschaft (estate guardianship). As detailed in legal analyses, if heirs are disputing shares or jointly abusing their access, like one child unilaterally revoking a parent’s old Vollmacht (power of attorney) to drain accounts, a court can appoint a neutral administrator to take full control.

This is the “nuclear” option. The court-appointed Verwalter (administrator) takes over, locking everyone out. They manage everything, from paying bills to running a family business, all at a steep hourly rate billed to the estate. “Sobald der externe Verwalter das Ruder übernimmt, sind die zerstrittenen Erben komplett entmachtet (As soon as the external administrator takes over, the feuding heirs are completely disempowered),” notes an inheritance lawyer. You lose all say. You just get the invoice.

The Escape Hatch: What You Can Do Today

This chaos is not inevitable. It’s a choice. Your choice. Here’s how to choose differently:

- Talk. Now. Have the awkward conversation. Outline your wishes. Explain the legal basics. It’s not about death, it’s about clarity and care. As one person who witnessed a peaceful inheritance process noted, grandparents who sorted things out in their 50s left behind “shared grief” and even a lovely family dinner tradition funded by leftover burial money, not lifelong bitterness.

- Get a Notar (Notary) Involved. A handschriftliches Testament (handwritten will) is valid but shockingly easy to invalidate with a missing date or unclear phrasing. Go notariell. The cost is an investment in family peace. The notary ensures it’s legally ironclad and registered centrally.

- Appoint a Testamentsvollstrecker (Executor). This is your single most powerful tool. As authorities themselves advise: “Setzen Sie deshalb im Testament oder Erbvertrag eine Willensvollstreckerin ein (Therefore, appoint an executor in your will or inheritance contract).” This person, a trusted friend, a lawyer, a neutral third party, ensures your will is executed as written. They mediate, they distribute, they handle the Finanzamt. They prevent the circus from starting.

- Document Everything. Keep a clear inventory of assets, accounts, and debts. Note any early gifts or loans. Store it with your will. Secrecy breeds suspicion.

- Consider Zukunftsvorsorge (Future Planning). For business owners or those with complex assets, tools like a Familienverein (family association) can hold assets collectively, preventing fragmentation. Others use Nießbrauch (usufruct) or Wohnrecht (right of residence) clauses to allow a surviving spouse to live in the home while ownership passes to children, avoiding forced sales.

Start planning today. Not because you’re morbid, but because you’re pragmatic. Because the greatest inheritance you can leave isn’t measured in euros, but in the continued peace and connection of the people you love. For those who do receive an inheritance, navigating what comes next is its own challenge, requiring smart strategies for investing inherited capital to secure its future. And while we often focus on inheritance itself, it’s part of a larger financial landscape, including the impact of generational property transfers on the broader housing market. Your foresight now can prevent a costly, painful battle later, one your family shouldn’t have to fight.