You got the promotion. The €85,000 salary is finally yours. You crack open a Gösser to celebrate, mentally calculating the extra €800 net that should hit your account each month. But when the first payslip arrives, the number is… underwhelming. Where did the money go? The culprit isn’t just the Finanzamt (Tax Office), it’s the Beitragsbemessungsgrenze (contribution assessment ceiling) that just crept up again, swallowing your raise before it ever reached your wallet.

This isn’t a bug. It’s the feature of Austria’s social security system that nobody talks about at parties.

The Ceiling That Keeps Rising (Whether You Like It or Not)

Here’s the raw deal: Austria’s Sozialversicherung (social insurance) contributions are tied to income ceilings that adjust annually. In theory, these adjustments follow wage growth and inflation. In practice, they’ve been sprinting ahead like someone stole their wallet.

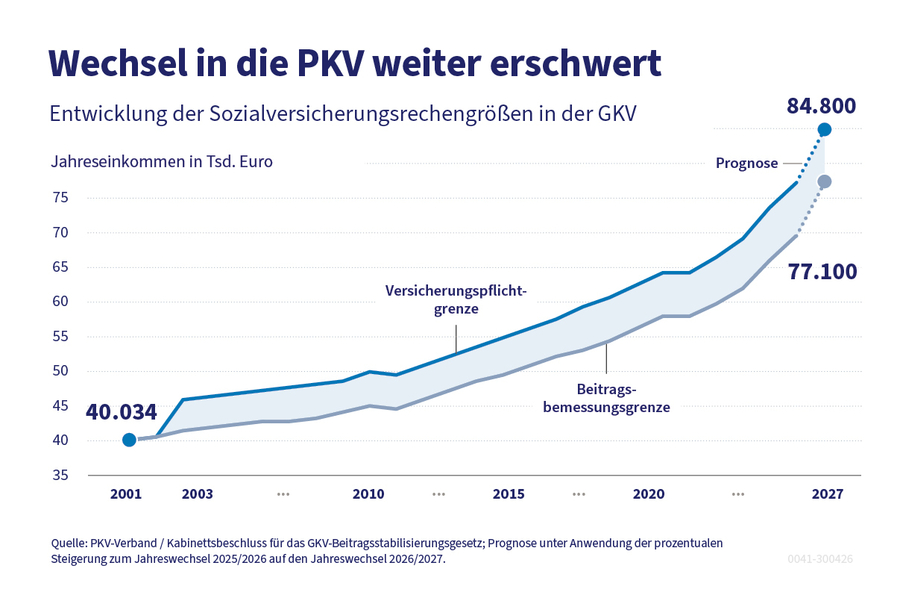

Between 2017 and 2027, the Versicherungspflichtgrenze (insurance obligation threshold) in neighboring Germany jumped 47%, from €57,600 to €84,800. Austria’s trajectory looks eerily similar. The ÖGK (Austrian Health Insurance) quietly announced that the 2027 Beitragsbemessungsgrenze will increase by an additional €300 per month on top of the regular adjustment.

That means if you earn above €6,425 monthly (€77,100 annually), you’ll suddenly pay contributions on more of your income. The previous ceiling already captured most white-collar workers. Now it’s reaching deeper into the “Mittelstand” (middle class) that politicians claim to protect.

The math stings. Someone earning €85,000 brutto will see their ÖGK contributions jump approximately €119 per month in 2027. That’s €1,428 annually, vanished. And unlike income tax, this isn’t funding roads or schools. It’s propping up a system where 80% of citizens receive more in benefits than they contribute.

Why Your Raise Is Actually a Pay Cut

Let’s get specific. Meet Thomas, a 34-year-old software engineer in Graz who just negotiated his salary from €75,000 to €85,000. He expected €500 more net per month. Instead, he gets €320. Why?

- Regular income tax: Takes a predictable bite

- Lohnsteuer (wage tax): No surprises there

- ÖGK contributions: Now calculated on €9,000 more income due to the ceiling hike

- Pension insurance: Same story, different acronym

The result? Thomas’s marginal tax rate on that “raise” exceeds 50% when you factor in the stealth social security grab. He’s working the extra hours, but the system is taking more than half the reward.

This is the impact on net salary that catches high earners off guard. You think you’re climbing the ladder, but the rungs are greased with Sozialversicherung contributions.

The Fairness Problem Nobody Wants to Solve

The Reddit thread on this topic exploded with a simple observation: Austria’s 56% state quota means the top 30% of earners fund 70% of income taxes and social contributions. Meanwhile, someone with a million in assets can self-insure through ÖGK for pocket change while paying minimal Kest (capital gains tax) by drawing down little income.

Universe A

You work 50 hours, earn €85,000, pay €35,000 in taxes and social contributions, and struggle to save for a down payment on a €400,000 Altbau (old building apartment) in Vienna’s 10th district.

Universe B

You inherited a paid-off Wohnung (apartment) in Döbling, live on €25,000 annual investment income, pay negligible social contributions, and still qualify for Zuschüsse (subsidies) because your “income” is low.

A friend of mine in Universe B recently told me it’s “fair” that I pay more because I “earn more.” When I pointed out he doesn’t earn less, he simply works less, he called me jealous. That’s the logic we’re dealing with.

The system taxes labor brutally while barely touching wealth. And the burden of social security contributions on retirement savings makes building wealth through work nearly impossible for the middle class.

The Political Magic Trick: Spending Without Accountability

Politicians love this ceiling hike because it’s invisible. They don’t have to vote for a tax increase. They don’t have to explain why ÖGK costs keep ballooning. They just let the automatic adjustment do the dirty work.

The research shows that between 2026 and 2027, Germany’s Beitragsbemessungsgrenze will jump from €69,750 to €76,350, a 9.6% increase. Austria follows the same playbook. The justification? “System stability.”

But here’s what they won’t say: ÖGK’s administrative costs have grown faster than patient care. The number of Verwaltungsbeamte (administrative officials) has exploded while service quality stagnates. You’re not paying more for better healthcare. You’re paying more for more bureaucracy.

What Actually Hits Your Wallet in 2027

| Your Brutto Salary | Current Monthly ÖGK | 2027 Monthly ÖGK | Difference |

|---|---|---|---|

| €65,000 | €487 | €487 | €0 (below ceiling) |

| €75,000 | €562 | €595 | +€33 |

| €85,000 | €638 | €757 | +€119 |

| €100,000 | €638 | €757 | +€119 (at ceiling) |

Note: Calculations based on 7.65% health insurance rate and 2027 ceiling increase

The kicker? Once you hit the ceiling, every euro above it is taxed at 42% or 48% income tax without any social insurance obligation. The system essentially says: “Congratulations, you’ve made it. Now give us half.”

The Escape Routes (And Why Most Are Blocked)

You could try switching to private insurance, but Austria’s Versicherungspflichtgrenze (insurance obligation threshold) is designed to keep you trapped. Unlike Germany’s two-tier system, Austria makes exiting ÖGK nearly impossible for employees. Self-insurance? Only if you have substantial wealth and can prove it.

The few who do escape face another trap: Private Krankenversicherung (private health insurance) premiums that rise with age, while ÖGK contributions are legally capped. At 30, private looks cheap. At 60, it’s a luxury.

Many international residents report waiting weeks for ÖGK appointments in Vienna, despite Austria’s reputation for efficiency. The system is cracking under its own weight, and your contributions are the duct tape.

The Bottom Line: Your Financial Planning Just Changed

Here’s what you need to do this month:

- Recalculate your net salary with the new 2027 ceiling. Use the impact calculator to see your real number.

- Negotiate differently. That €5,000 raise? Ask for €3,000 plus €2,000 in employer pension contributions or a company car. Benefits aren’t subject to ÖGK contributions.

- Max out your Vorsorge (provision). Every euro you put in a betriebliche Vorsorge (company pension plan) reduces your Beitragsgrundlage (contribution base). It’s the only legal way to opt out of the system robbing your raise.

- Consider your Wohnsitz (residence). Lower Austrian provinces have slightly different rules. Vienna’s high salaries mean you’re hitting ceilings faster than someone in Burgenland.

- Track your Grenze (threshold). If you’re within €5,000 of the ceiling, every bonus or 13th/14th salary payment gets hit with the full social security rate. Time your income.

The uncomfortable truth? Austria’s Sozialversicherung system works brilliantly for the 80% who take out more than they put in. For the 20% funding the party, it’s a wealth tax disguised as solidarity.

Your raise didn’t disappear. It was redistributed before you ever saw it. And the most frustrating part? Nobody asked. They just changed the numbers and called it “adjustment.”

Welcome to Austria, where the mountains are high, the bureaucracy is higher, and your net salary is always one policy change away from shrinking.