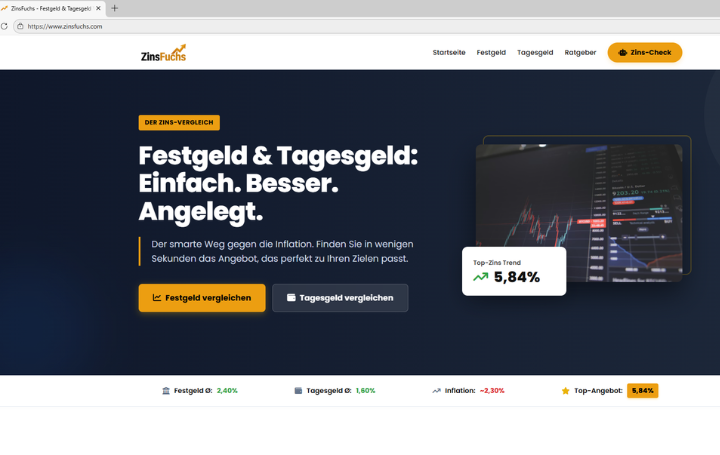

You’re scrolling through your phone at 11 PM, comparing Festgeld (fixed-term deposit) rates because your Erste Bank advisor told you, again, that 1.2% is “very competitive for the current market.” Then you see it: 5.84% per year for a 12-month deposit. Five point eight four. The number glows on your screen like a neon sign in a dark Vienna alley. Your brain does the math. On €10,000, that’s €584 in interest instead of €120. That’s a weekend in Paris. That’s your Kaution (security deposit) for the next Altbau apartment. That’s free money, right?

Wrong. That’s exactly how they get you.

The website looks legitimate. Professional design, comparison tables, financial advice articles. It even mentions real banks like KBC. But here’s the thing: that Zinsfuchs.com page promising you the moon? The company behind it, ZinsFuchs GmbH, doesn’t exist. Not in the Handelsregister (commercial register). Not in the FMA (Financial Market Authority) database. Not anywhere except on that slick website designed to separate you from your savings.

The Anatomy of a Festgeld Scam: Why 5.84% Is Financially Impossible

Let’s get technical for a second. Festgeld rates in Austria are tied to the European Central Bank’s policies, bank liquidity, and actual market conditions. When legitimate Austrian government bond rates barely touch 2% and even the best Tagesgeld accounts hover around 1.5%, a 5.84% fixed rate is about as realistic as finding a cheap Altbau in the first district.

The scammers behind sites like zinsfuchs.com understand Austrian savers’ psychology perfectly. We’re a nation of prudent investors who grew up with Bausparen (building savings contracts) and Sparkonten (savings accounts). We trust fixed interest. We love security. And we’re desperately searching for yield in a low-rate environment that feels like it’s suffocating our financial goals.

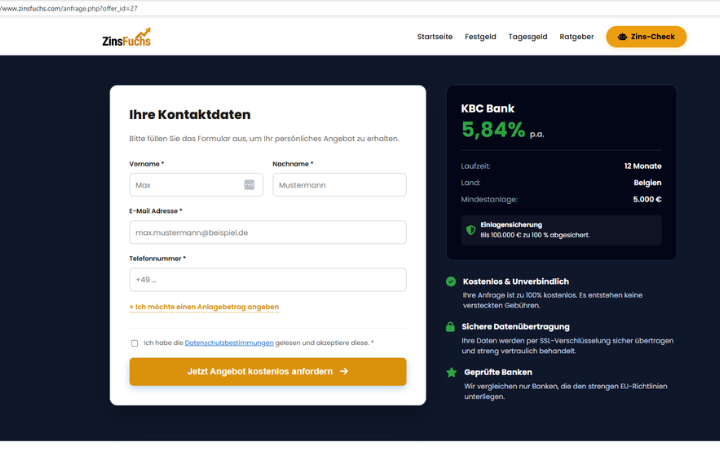

The site shows you exactly what you want to see: comparison tables where their fake product outperforms real banks by 3-4 percentage points. They’ll even tell you to “verify the provider”, knowing most people won’t dig deep enough. The contact form asks for your name, phone number, email, and “additional sensitive information.” Once you submit that? You’re not getting a Festgeld account. You’re getting added to a call list where “financial advisors” (read: professional scammers) will pressure you to transfer money to accounts that disappear faster than a Wiener Linien ticket inspector when you need one.

Red Flags That Scream “Betrug” (Fraud)

1. The Interest Rate Fantasy

If it sounds too good to be true, it violates Austrian banking law. Real banks operate with razor-thin margins. When neobroker security differences show how even legitimate fintechs struggle to offer 2% on deposits, a 5.84% Festgeld rate is mathematically impossible without taking massive risks, risks that would legally require them to disclose you’re basically investing in junk bonds or worse.

2. The Ghost Company

Always check the FMA Unternehmensdatenbank (company database). Legitimate Austrian financial institutions must register with the Finanzmarktaufsicht. The process takes months and costs thousands. Scammers skip this step because they know their operation won’t last that long. A quick search for “ZinsFuchs GmbH” returns nothing. That’s not a oversight, that’s a death sentence for your investment.

3. The Data Harvesting Form

Real Austrian banks don’t ask you to submit personal data through third-party comparison sites to “access” their rates. You go directly to the bank’s website, log in with your Bankomatkarte (debit card) reader, and open the product through their secure portal. If a site demands your phone number before showing you the actual offer, they’re building a contact list, not a banking relationship.

4. The Stolen Identity Game

Scammers increasingly steal real company identities. The BaFin (German regulator) recently warned about apps misusing legitimate company names like AL Konzept GmbH & Co. KG. In Austria, they’ll slap a real bank’s logo, like Easybank, on phishing emails claiming your “Sicherheitsprotokoll” (security protocol) needs updating. The email looks official, uses the right colors, but asks you to click a link that leads to a data-harvesting site. The Verbraucherzentrale (consumer protection center) has flagged multiple Easybank phishing campaigns where the only red flags are an impersonal greeting and a sender address that doesn’t quite match.

How the Scam Actually Works

You fill out the form on zinsfuchs.com. Within 24 hours, a “financial consultant” calls you, maybe from a Vienna number, maybe not. They speak perfect German, reference Austrian financial regulations, and explain how this “exclusive” Festgeld product works. They’ll email you documents that look official. They’ll even set up a “customer portal” where you can see your “investment” growing.

The portal is fake. The documents are forged. When you transfer your €5,000 minimum investment, it goes to a foreign account or gets converted to crypto within hours. When you try to withdraw after 12 months, suddenly there are “tax issues” or “compliance fees” requiring additional payments. This is the recovery scam phase, where they double-dip on your desperation.

The Verbraucherzentrale Nordrhein-Westfalen launched a “Fake-Check Geldanlage” tool specifically because these scams have evolved. The tool asks targeted questions about investment offers and flags typical warning signs: unrealistic returns, artificial time pressure, unsolicited contact, and blocked withdrawals.

Real Banks vs. Fake Banks: The Verification Checklist

Before you transfer a single Euro to any Festgeld provider, run through this Austrian-specific checklist:

Visit fma.gv.at and search their Unternehmensdatenbank. If the company isn’t listed, it’s not authorized to offer financial products in Austria. Period.

Real Austrian banks have physical branches. Even online-only banks like Easybank have a registered headquarters you can visit. Scammers use virtual offices or addresses that lead to mail forwarding services in Cyprus or Malta.

Legitimate banks never pressure you to invest via phone call. They don’t use WhatsApp groups to discuss “exclusive opportunities.” They certainly don’t threaten account deactivation if you don’t act within 48 hours.

Compare rates across legitimate savings product comparison sites like Finanz.at or through your existing bank. If one offer is more than 1% above the market average, it’s either a promotional rate for new customers (clearly disclosed and capped) or a scam.

Austrian websites legally require a proper Impressum (legal notice). Scammers either skip it, use a stolen one from a real company, or list a generic email and virtual phone number. Call the number. If it goes to voicemail after one ring or connects you to a call center asking for your “investment ID”, hang up.

Why Easybank Customers Are Prime Targets

Easybank, as Austria’s largest direct bank, gets impersonated constantly. Scammers know that Easybank customers are comfortable with online banking and rate shopping. The phishing emails are sophisticated, using the bank’s actual logo, mimicking their communication style, even referencing real regulatory changes like PSD2.

The Verbraucherzentrale has documented multiple campaigns where Easybank customers receive emails about “Sicherheitsprotokoll: Aktualisierung aktualisiert” (yes, the redundancy is a clue). The email states: “Dieser Vorgang ist verpflichtend, um eine temporäre Deaktivierung Ihres Online-Zugangs zu vermeiden.”

Real Austrian banks don’t write like this. They address you by name. They don’t threaten account closure in the first sentence. And they never, ever include a direct login link in an email.

What to Do If You’ve Already Been Scammed

First: Don’t panic. But act immediately.

- Contact your bank within 24 hours. If the transfer is still pending, they might be able to reverse it.

- File a police report at your local Polizeiinspektion. Austrian law enforcement takes financial fraud seriously, especially cross-border cases.

- Report to the FMA through their online whistleblower portal. This helps them track patterns and warn others.

- Document everything. Screenshots, emails, phone numbers, account details. Scammers often reuse elements that investigators can trace.

- Beware the recovery scam. Months later, someone claiming to be a “financial investigator” might contact you promising to recover your funds, for a fee. This is the same criminals coming back for seconds. Real authorities like the Bundeskriminalamt never charge victims for investigations.

The Bottom Line: Austrian Financial Paranoia Is Justified

In Austria, we trust our banks like we trust our Apotheken (pharmacies). The system feels solid, regulated, safe. But that trust is exactly what scammers exploit. They know you’re tired of day-to-day deposit skepticism. They know you’re comparing rates because deceptive brokerage fee practices have made you suspicious of traditional providers.

The Festgeld scam works because it mimics the Austrian financial culture perfectly. It promises the security we crave with returns we dream about. But real Austrian financial security comes from boring, predictable, regulated institutions, not from a website you found at midnight promising to triple your interest income.

So the next time you see that 5.84% rate, do what any sensible Viennese would do: close the tab, make yourself a Melange, and check the FMA database in the morning. Your future self will thank you, and so will your still-intact savings account.