You know that sinking feeling when you check your business account at quarter-end? The one where you’ve mentally calculated your profit, maybe even planned a small investment or, gasp, a weekend away, only to find €47.30 in mystery fees has evaporated into the banking ether? Welcome to the Austrian Geschäftskonto (business account) reality, where your quarterly earnings become someone else’s predictable revenue stream.

Let me paint you a picture. You’re a freelance graphic designer in Graz, finally hitting your stride. You’ve landed three solid clients, your Einnahmen-Ausgaben-Rechnung (income-expenditure statement) looks crisp, and then, bam, your Erste Bank statement arrives. Fifty euros. Every. Single. Quarter. For what? The privilege of them holding your money while you hustle for it. And here’s the kicker: you’re not alone. That Reddit thread where a sole proprietor posted their Erste Bank quarterly breakdown? The comments exploded. One user suggested bank99 at €5 monthly “all in”, while another countered that the customer service felt like “-99.” The battle lines were drawn: cheap versus usable.

The Austrian Business Banking Trap: It’s Not Optional

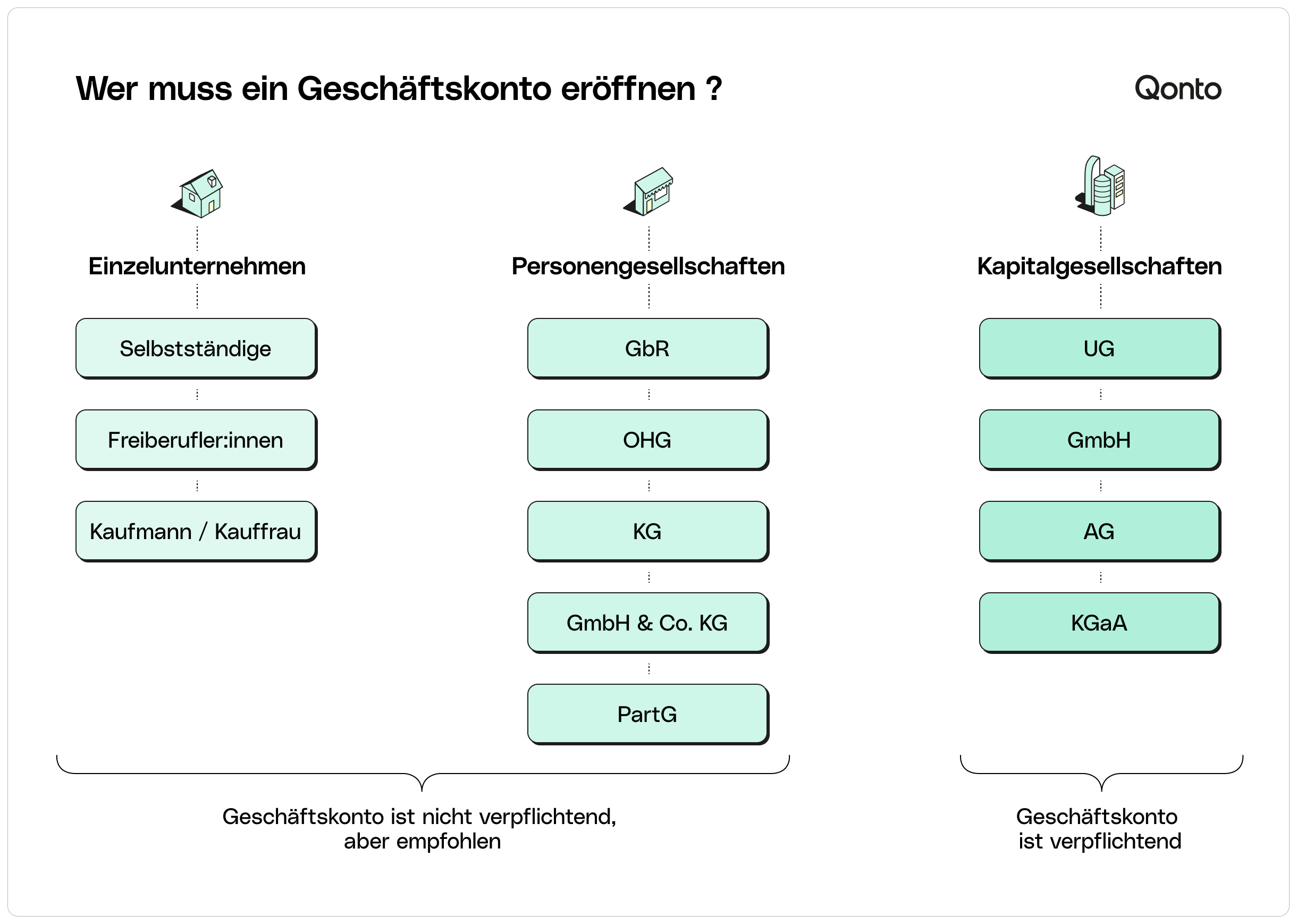

Unlike in Germany where you might squeak by mixing private and business funds, Austria plays hardball. The law mandates a Kommerzkonto (commercial account) for any gewerbliche Tätigkeit (commercial activity). Even as an Einzelunternehmer (sole proprietor) or Freiberufler (freelancer), you’re legally required to separate your business finances. The Finanzamt (Tax Office) expects clean books, and trust me, they notice when your coffee expenses mingle with client invoices.

Traditional Austrian banks, Erste Bank, Bank Austria, Raiffeisen, BAWAG, know this. They’ve built their business account pricing like a Viennese café menu: reasonable base price, but the Sachertorte of services costs extra. Your quarterly €50 might include the account fee, sure, but then you get nickeled and dimed on everything beyond basic SEPA transfers. Need a physical card? That’s extra. Cash deposit at a branch? Extra. More than 50 transactions monthly? Welcome to per-booking fees that make you question every invoice payment.

The research from sevdesk cuts through the noise: “Um Kosten zu sparen, könntest du als Geschäftskonto zunächst auch ein zweites Privatgirokonto führen” (To save costs, you could initially use a second private checking account as your business account). But, and this is crucial, your bank’s AGB (terms and conditions) probably prohibit this. Many Austrian banks tolerate it only until your transaction volume triggers their compliance alarm. Then they either force you onto a business tariff or show you the door.

Why “Free” Business Banking Is a Beautiful Lie

Neo-banks and fintechs have swooped in promising salvation. Qonto, Finom, N26, Fyrst, they all offer “free” business accounts. The marketing screams zero fees, but the fine print whispers expensive secrets.

Take Finom Solo. Zero monthly fee, sure. But exceed €2,000 in monthly revenue and suddenly you’re paying 0.3% on every additional euro. For a growing business, that quarterly “free” account becomes a percentage-based vacuum. N26 Business Standard gives you five free SEPA transfers monthly. The sixth costs you. Need to deposit cash? Good luck. Most fintechs don’t even offer it, and those that do charge rates that would make a Wechselstuben (exchange office) blush.

The Handelsblatt comparison reveals the truth: only five providers offer genuinely free accounts, Finom, N26, FYRST, Kontist, and GRENKE. But each comes with a transaction ceiling. FYRST gives you 75 free SEPA transactions monthly, which sounds generous until you’re paying suppliers, receiving client payments, and handling subscriptions. Cross that threshold and each additional booking costs €0.08. That doesn’t sound like much until you do 150 transactions in a busy month and suddenly owe €6 extra. Over a quarter? That’s €18 you didn’t budget for.

The Hidden Quarterly Costs That Actually Matter

Let’s get specific about where your money leaks. These aren’t the headline fees, they’re the death-by-a-thousand-cuts charges that show up every three months:

1. The Transaction Limit Trap: Your “free” account includes 50 monthly bookings. You hit 67 because a client paid in installments and you had three extra supplier bills. At €0.30 per extra transaction, that’s €5.10 monthly, or €15.30 quarterly. Pure profit for the bank.

2. Cash Handling Punishment: You’re a craftsperson selling at markets. That €800 in weekend cash? Depositing it at a branch costs 1.5%, €12. Do this twice a quarter and you’ve handed over €24 for the privilege of putting your own revenue in the bank. FYRST charges just €0.01 per deposit, but you need to find a Deutsche Bank branch. In rural Austria, that might be a 40-minute drive.

3. Foreign Transaction Gouging: Client in Switzerland pays you €1,500. Your “free” account hits you with a 1.5% foreign transaction fee. That’s €22.50 gone, and you haven’t even converted the currency. Revolut and Qonto offer better rates, but their free tiers limit monthly foreign transaction volumes.

4. Card Replacement Extortion: Lost your business debit card? Replacement fees range from €10 to €25 depending on the provider. Some Austrian traditional banks charge extra for “expedited” shipping that still takes a week.

5. The Inactivity Gotcha: Kontist Free charges €2 monthly for inactive accounts. Forget about that side-project account you opened but haven’t used yet? After three months, you’ve paid €6 for nothing.

6. Software Integration Fees: Need to connect your account to sevdesk or another Buchhaltungssoftware (accounting software)? Some banks charge €5-10 monthly for API access. Others bundle it “free” but limit the number of transactions that sync.

The Neo-Bank Reality Check: Who Actually Saves Money?

After analyzing the data, here’s the uncomfortable truth: the right choice depends entirely on your business model, not the marketing.

For digital freelancers (web designers, consultants, translators): Qonto’s free tier or N26 Business Standard works. You rarely handle cash, mostly receive SEPA transfers, and stay under transaction limits. Your quarterly cost? Potentially zero, if you’re disciplined.

For market traders and craftspeople: The fintech dream falls apart. You need cash deposits, and lots of them. FYRST’s partnership with Deutsche Bank gives you access to the Cash Group network, but you’ll pay €10 monthly after the first year. Still cheaper than Raiffeisen’s €15 plus deposit fees. Your quarterly cost: €30, but predictable.

For growing startups: That 0.3% revenue-based fee from Finom becomes catastrophic as you scale. At €10,000 monthly revenue, you’re paying €30 monthly in fees alone, €90 quarterly. Suddenly, Raiffeisen’s €50 flat fee looks reasonable. The key is knowing your breakpoint.

For side hustlers: Using a second private account at a bank like bank99 (€5 monthly all-in) might work temporarily. But remember: the Finanzamt wants clean separation. During a Betriebsprüfung (business audit), mixed accounts raise red flags. The auditor’s time costs you more than any bank fee.

Practical Strategies to Slash Quarterly Banking Costs

Enough theory. Here’s how to actually keep that money in your pocket:

Audit Your Last Three Statements: Not the summary, the detailed PDF. Highlight every fee. You’ll likely find charges you didn’t know existed. One Vienna-based consultant discovered €18 quarterly in “paper statement fees” she could eliminate by switching to online-only.

Calculate Your True Transaction Volume: Count every booking, incoming, outgoing, SEPA, standing orders. Don’t guess. Most entrepreneurs underestimate by 30%. If you’re consistently over limits, a flat-fee account is cheaper.

Negotiate with Your Traditional Bank: Yes, really. That Reddit user who contacted Erste Bank through their George app and asked for new conditions? It works. Banks retain business customers aggressively. Mention you’re considering Qonto or Finom. Suddenly, €50 quarterly becomes €35. It’s not great, but it’s €60 yearly savings for a 10-minute call.

Leverage the Kontowechselservice (Account Switching Service): Qonto and others offer free switching services. They handle moving your standing orders and informing clients. The mental barrier to switching is high, this eliminates the excuse.

Use Sub-Accounts Strategically: Most fintechs offer free sub-accounts. Create one for VAT (Umsatzsteuer), one for income tax (Einkommensteuer), and one for operating expenses. This doesn’t directly save bank fees, but it prevents the cash flow crunches that force you into expensive overdrafts.

Time Your Cash Deposits: If you must use a bank that charges for cash, deposit less frequently but in larger amounts. Five deposits of €200 each might cost €15, while one deposit of €1,000 costs €3. That’s €12 quarterly savings for minimal effort.

The Cash Flow Hack That Actually Matters

Here’s where we connect to that internal link about cash flow. The real cost of banking fees isn’t the money leaving your account, it’s the opportunity cost of that money not working for you. Every euro paid in fees is a euro not invested in tools, marketing, or, let’s be honest, your sanity.

Strategies to avoid unnecessary bank fees and optimize cash flow work because they treat banking as a variable cost to be managed, not a fixed expense to be endured. When you route client payments to accounts with higher free transaction limits, you’re not just saving €15 quarterly, you’re maintaining control over your working capital.

When Free Actually Means Free (And When It Doesn’t)

The only scenario where a truly free business account exists? You’re a digital-native sole proprietor with:

– Under 50 transactions monthly

– Zero cash handling

– No foreign transactions

– Patience for limited customer support

If that’s you, N26 Business Standard or Qonto Starter will cost you exactly €0 quarterly. But add one cash deposit, one foreign client, or one busy month, and the fee cascade begins.

For everyone else, the honest answer is: budget €30-60 quarterly for banking. The goal isn’t zero fees, it’s predictable, minimal fees that don’t scale with your revenue. A flat €15 monthly fee hurts less than a 0.3% revenue tax disguised as “free banking.”.

Your Action Plan Before Next Quarter

- This week: Download three months of statements. Calculate your actual transaction volume, cash deposits, and foreign payments.

- Next week: Use the Handelsblatt comparison tool (or Qonto’s calculator) to model your costs across five providers. Include your time value, €30 saved isn’t worth 5 hours of customer service calls.

- This month: Open a secondary account at a fintech. Don’t switch yet, test it with 20% of your transactions. See if the “free” promise holds.

- Before quarter-end: Make your decision. Either negotiate with your current bank or pull the switch trigger. The Kontowechselservice makes this painless.

The Austrian banking system, like a Viennese coffee house, runs on tradition and hidden rules. Your Geschäftskonto doesn’t have to be a quarterly mystery novel of disappearing funds. With the right setup, you can make those fees as predictable as your morning Melange, and potentially just as affordable.

Just don’t wait for your bank to volunteer the savings. They’re too busy counting their quarterly profits. Yours.