Here’s what your bank won’t tell you while you’re busy collecting loyalty points: Swiss travelers are bleeding money through card choices that feel smart but mathematically stink. The fresh Moneyland study just dropped the numbers, and they’re brutal. For a typical CHF 3,000 vacation budget, the difference between the smartest and dumbest card choice is CHF 179. That’s a flight to Lisbon you just handed to your bank.

The Debit vs. Credit Massacre

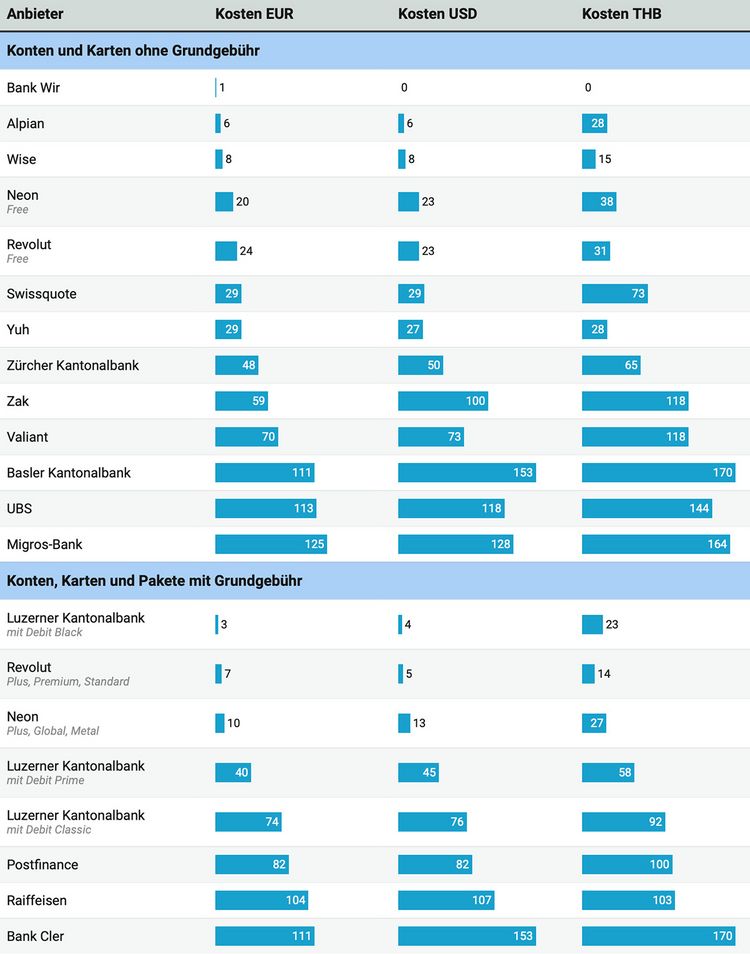

Let’s cut through the marketing fluff. Moneyland analyzed 35 payments totaling CHF 3,000 across different currencies. The results? Debit cards cost between CHF 1 and CHF 170. Credit cards? CHF 25 to CHF 180. This isn’t a rounding error, it’s a systematic wealth transfer from vacationers to bank shareholders.

The mechanics are simple but ugly. Every time you swipe abroad, you’re hit with two invisible taxes: a Devisenkursaufschlag (exchange rate markup) and transaction fees. Most Swiss residents focus on the annual card fee (CHF 0 vs. CHF 100) while ignoring the 1.5% to 2% currency conversion spread that actually drives costs. It’s like comparing cars by their sticker price while ignoring fuel consumption.

The Unlikely Champion: Bank WIR

Plot twist: the cheapest card for foreign payments isn’t from a hip fintech startup or a banking giant. It’s from Bank WIR, the Basel cooperative bank that most international residents have never heard of. For EUR purchases, you’ll pay exactly CHF 1 in fees on that CHF 3,000 budget. For USD or Thai Baht? Zero. Nothing. Nada.

This isn’t a gimmick. Bank WIR operates on a different model, cooperative, not profit-maximizing. While UBS and Credit Suisse (now UBS, thanks to that little 2023 merger) are charging CHF 113-118 for the same EUR transactions, this sleepy Basel institution is basically giving you the interbank rate. The catch? You need to live in their catchment area and open an actual relationship, not just a digital wallet.

Neo-Banks vs. The Dinosaurs

The fintech evangelists aren’t entirely wrong. Alpian (CHF 6) and Wise (CHF 8) absolutely crush traditional banks on foreign debit card fees. Neon Free at CHF 20 and Revolut Free at CHF 24 still beat most incumbents by a factor of 5. These players built their systems without the legacy infrastructure that makes foreign exchange a profit center rather than a service.

But here’s where it gets spicy: the traditional banks aren’t taking this lying down. The Luzerner Kantonalbank Debit Black card costs just CHF 3 for that EUR vacation, beating every neo-bank except Bank WIR. The catch? You’ll pay a CHF 200+ annual fee for the privilege. Do the math: you need to spend over CHF 6,800 abroad annually just to break even versus using Wise for free.

This creates a perverse incentive structure. The “premium” cards with “better” foreign rates are actually wealth extraction devices for the banking class. They dangle low foreign fees in front of high-income travelers while collecting fat annual fees that subsidize the entire operation.

The Credit Card Conundrum

“But I need a credit card for rental cars and hotels!” Absolutely correct. The Moneyland study confirms what every expat learns the hard way: you can’t travel with just a debit card. The solution isn’t abandonment, it’s strategic deployment.

Among kostenlose Kreditkarten (free credit cards), the new Swisscard Visa (launched autumn 2025) is the least terrible at CHF 55 for our EUR scenario. The worst? Swisscard’s own Cashback and Poinz cards at CHF 146. Yes, the same issuer sells both the best and worst free cards. Let that sink in.

For those willing to pay annual fees, UBS Key4 credit card costs CHF 25 in foreign fees, substantially better than any free option. But again, you’re paying CHF 100+ annually for the card itself. The break-even versus Swisscard Visa? Around CHF 3,000 in foreign spending per year.

The Multi-Currency Hack Nobody Talks About

Here’s the pro move that Moneyland’s analysis barely mentions: Währungskonten (multi-currency accounts). Alpian, Revolut, Swissquote, Wise, and Yuh let you hold actual EUR, USD, GBP balances. When you pay in a currency where you hold funds, zero conversion happens. The fee disappears entirely.

This transforms the game. Instead of optimizing for the lowest 1.5% markup, you’re paying 0%. For frequent travelers or remote workers earning in foreign currencies, this is the financial equivalent of finding a Zürich apartment without a Mietkaution (rental deposit).

The catch? You need to fund these accounts. Wise gives you the best exchange rates for conversion, but you’re still paying something to get CHF into EUR. The real magic happens if you receive income directly in foreign currency.

The Thai Baht Massacre

Currency choice matters more than your card choice. The Moneyland study tested EUR, USD, and Thai Baht. Baht is where banks get predatory. While EUR fees range from CHF 1-125 for debit cards, Baht fees hit CHF 0-170. Bank WIR again charges zero for Baht, while traditional banks like UBS and Migros Bank spike to CHF 144-164.

Why? Exotic currencies have wider spreads and less liquidity. Banks exploit this information asymmetry. You can’t mentally calculate the fair CHF/THB rate, so they pad it aggressively. The solution: if you’re heading to Southeast Asia, load up a multi-currency account with USD (more widely accepted) and use that instead.

Cash Withdrawals: The Ultimate Rip-Off

Moneyland calculated cash withdrawal costs for CHF 3,000 in twelve transactions. The brutal truth: it was never cheaper to withdraw cash than paying directly by card. Not once.

Debit cards cost CHF 25-180 for these withdrawals. Credit cards? CHF 150-250. That ATM you see in every Thai 7-Eleven is a profit center for someone, and it’s not you.

The advice is clear: withdraw minimal cash for emergencies only, using your cheapest debit card (Bank WIR at CHF 25 max). Never use a credit card at an ATM unless you enjoy paying 8% effective interest from day one.

Your Actual Strategy for 2026

- Get a Bank WIR account if you’re in their region. Their debit card is the undisputed champion.

- If not, open Wise for free. Their debit card costs CHF 8 on CHF 3,000, still 90% cheaper than most traditional banks.

- Add Neon Free as a backup. CHF 20 isn’t terrible, and their app actually works.

- For credit cards, grab the Swisscard Visa (free) for hotels and rentals. Accept the CHF 55 foreign cost as a necessary evil.

- If you spend >CHF 10k abroad annually, consider Neon Plus (CHF 24/year, zero foreign fees) or UBS Key4 (if you already bank with UBS).

- Never, ever accept terminal conversion to CHF abroad. That’s a 5-7% hidden fee.

- Never withdraw cash with a credit card. That’s financial self-harm.

The Bigger Picture: Why Swiss Banks Get Away With This

Swiss residents paid CHF 24.9 billion abroad with credit cards versus CHF 15.4 billion with debit cards in 2025, according to SNB data. Yet debit cards just overtook credit cards in transaction count for the first time. Translation: we’re using debit cards for small stuff but still reaching for credit cards for big purchases, exactly backwards.

Banks maintain this through strategic confusion. They advertise “free” cards while hiding currency markups. They create complex fee structures requiring spreadsheets to compare. They train staff to emphasize points and insurance over the actual cost of transactions.

The Moneyland study cuts through this fog. The question is whether you’ll act on it, or keep funding your banker’s bonus because changing cards feels like too much trouble.

Your move. That flight to Lisbon is waiting.