You’re doing everything right. Monthly savings plan, broad market ETF, compounding returns. Then January rolls around, and your broker casually informs you: “You owe us taxes on gains you don’t have yet.”

Welcome to the Vorabpauschale (pre-tax levy), Austria’s special way of making you feel like your ETF is a high-maintenance friend who charges you rent before you’ve even moved in.

The concept is brutal in its simplicity: you pay taxes on theoretical gains before you actually sell anything. It’s like the Finanzamt (Tax Office) heard about compound interest and decided to show up to the party before it even started.

The Anatomy of a Tax That Makes No Sense (Until It Does)

Let’s be honest: the Vorabpauschale (pre-tax levy) sounds like something a finance minister invented after three glasses of Grüner Veltliner. A tax on unrealized gains? On funds that haven’t paid you a single cent?

Here’s the logic, such as it is: the Austrian tax system assumes that if your accumulating (thesaurierender) ETF grows, it must be generating income internally, reinvesting dividends, issuing shares, whatever. The system doesn’t care that you haven’t touched a euro of it. It wants its 27.5% KESt (Kapitalertragsteuer, or capital gains tax) now.

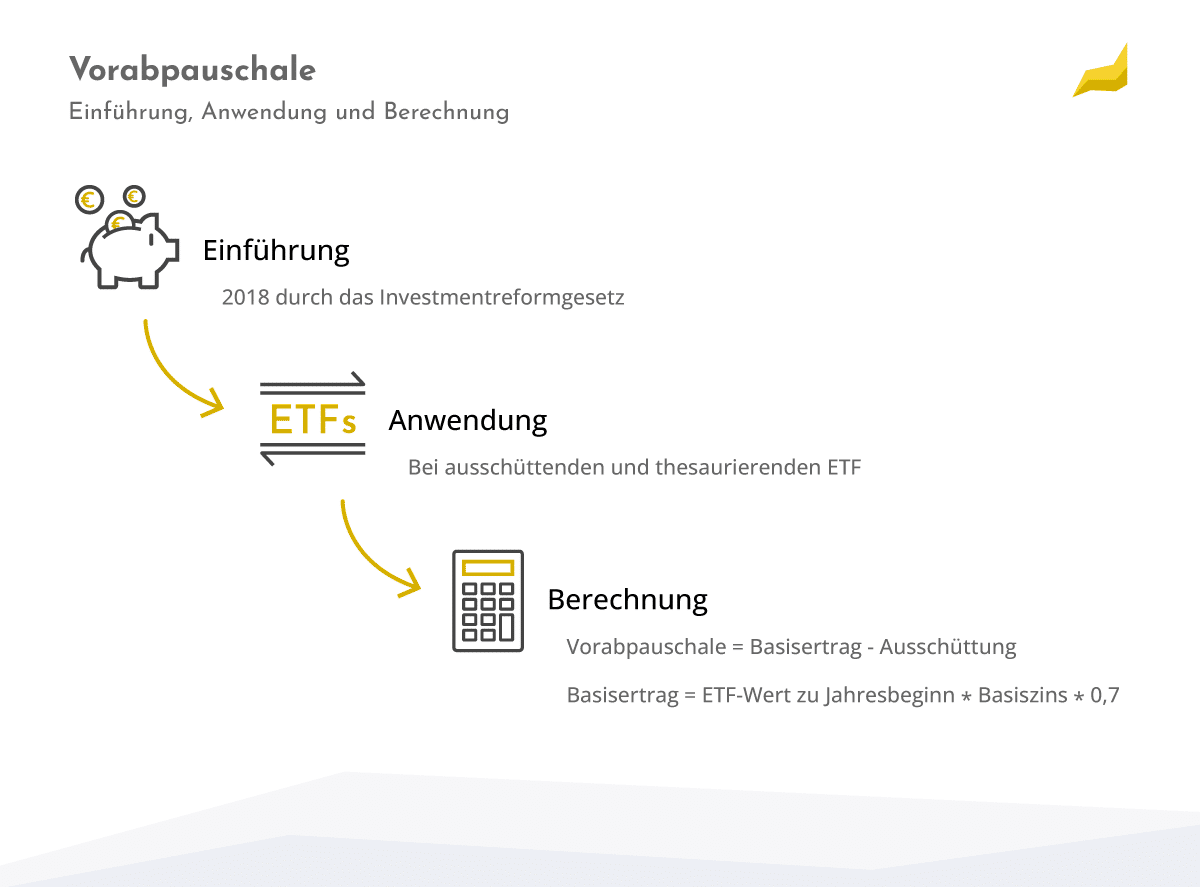

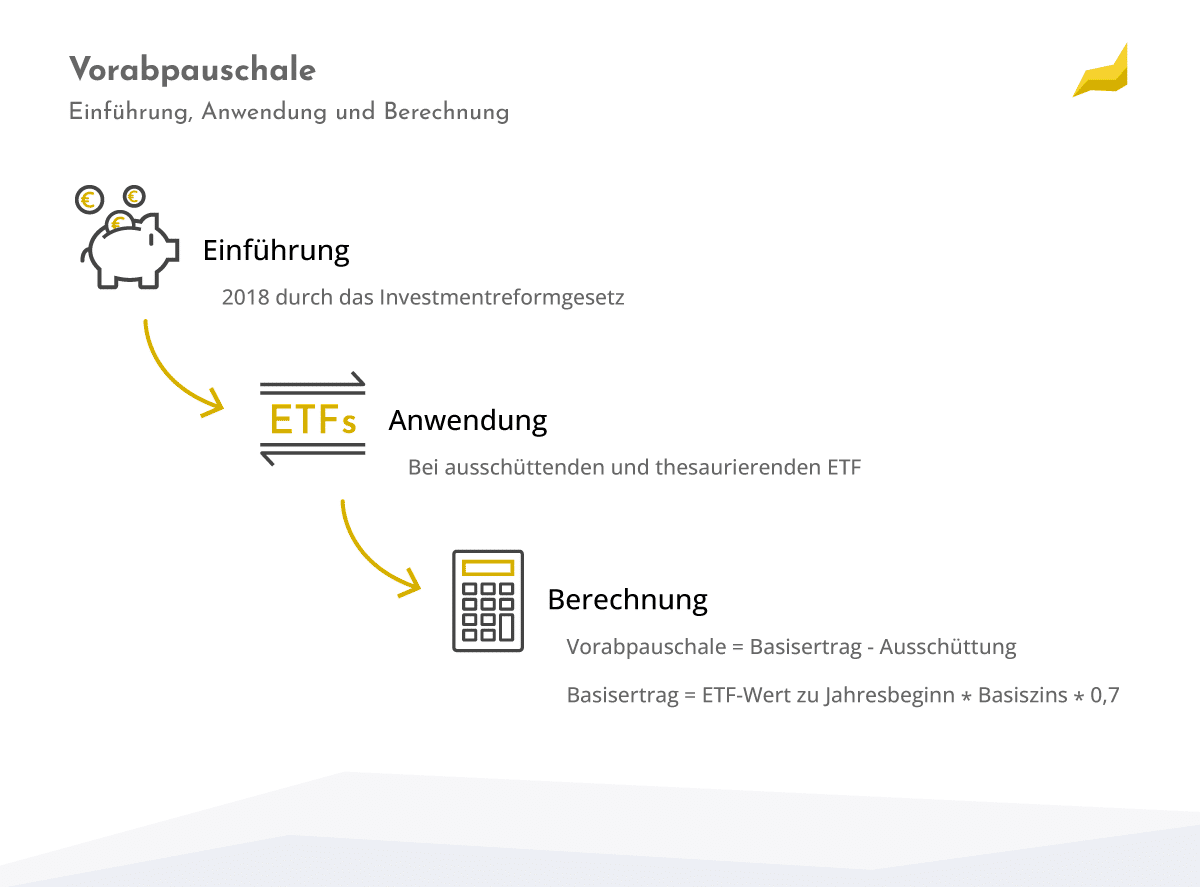

The calculation is a masterpiece of bureaucratic gymnastics. It starts with the Basisertrag (base yield), which is 70% of the annual base interest rate (set by the German finance ministry, because of course it is), multiplied by the fund’s value at the start of the year.

Then they compare this fictional yield against your fund’s actual growth. Whatever is lower becomes your taxable base. If your ETF goes up 15% but the base yield is only 2%, congrats, you’re only taxed on the 2%. If your ETF drops in value? The Vorabpauschale (pre-tax levy) can’t be negative, so you pay… nothing. Small mercies.

The Numbers That Matter Right Now

Here’s where the topic gets spicy. After years of near-zero base interest rates where the Vorabpauschale (pre-tax levy) was basically a ghost tax, the world has changed. The base interest rate for 2026/2027 is set at 3.20%.

Let me run that through the calculator for you.

Say you have €50,000 in a global ETF. The base yield is:

€50,000 × 3.20% × 70% = €1,120

Then factor in the Teilfreistellung (partial exemption), a 30% exemption for equity funds (Aktienfonds). So your taxable amount drops to €784. At 27.5% KESt (capital gains tax), that’s €215.60 in taxes on gains you haven’t realized.

That’s €215.60 the taxman takes before you’ve sold a single share.

You can check your potential burden using tools like the AAV Vorabpauschale Rechner, which calculates this automatically based on your fund category and investment volume.

The Silent Killer: Why This Changes Everything

I’ve seen investors compare ETFs purely on the TER (Total Expense Ratio), that 0.07% difference between an iShares and an Xtrackers fund. But the Vorabpauschale (pre-tax levy) can easily dwarf your cost savings.

Here’s the problem most people miss: the compounding effect of early taxation.

When the taxman takes €215.60 from your account in January, that money disappears from your compounding machine. Over twenty years, at 7% annual growth, that single €215 loss costs you roughly €830 in future returns. Do that every year, and the gap widens into a canyon.

This is precisely why many Austrian investors use the Tranchenstrategie (Tranche Strategy) to optimize their tax burden in retirement. The strategy involves carefully timing purchases and sales to minimize the Vorabpauschale (pre-tax levy) impact over a lifetime.

Distributing vs. Accumulating: The Great Debate

If you’re Austrian and investing in ETFs, you’ve heard this question: “Should I choose the ausschüttend (distributing) or the thesaurierend (accumulating) version?”

The standard advice says distributing funds help you use your annual tax exemption (€7,370 for singles in 2026). But here’s the twist: distributing funds largely avoid the Vorabpauschale (pre-tax levy) .

When a fund pays out dividends, the tax is deducted at source. The Vorabpauschale (pre-tax levy) calculation subtracts those distributions from the base yield. If your distribution exceeds the base yield, which happens often, the pre-tax burden drops to zero.

This means that for many investors, especially those with smaller portfolios, distributing ETFs can be more tax-efficient. You pay taxes on actual income, not fictional gains. And you can control when to reinvest by either keeping the cash or buying more shares.

The Strange History Nobody Remembers

The Vorabpauschale (pre-tax levy) wasn’t always with us. It entered Austrian tax law as part of the 2018 Investmentsteuerreform (Investment Tax Reform), piggybacking on Germany’s framework. The idea was to prevent tax deferral on accumulating funds, closing a loophole where investors could let their money compound in growth funds for decades without paying a cent in taxes.

In those early years, with the base interest rate hovering around 0.07%, the tax was essentially a rounding error. Nobody cared. Then the ECB raised rates, and suddenly your ETF’s theoretical gains became very real tax burdens.

Many international residents find this system baffling. You can read more about the historic development of index funds and tax-simple brokers in Austria to understand how we arrived at this peculiar arrangement.

What You Can Actually Do About It

You can’t escape the Vorabpauschale (pre-tax levy). But you can manage it.

Keep cash in your account. Around mid-January, your broker will debit the tax. If your Verrechnungskonto (settlement account) is empty, they might sell off ETF shares to cover the cost, creating a realized gain that triggers more taxes. An expensive domino effect.

Use your Freistellungsauftrag (tax exemption order). If you have a tax exemption in place, your broker won’t deduct taxes until you exceed the limit. Handy, but remember: unused exemption space doesn’t roll over.

Consider distributing ETFs for your taxable account. Especially if you’re in the accumulation phase. The tax drag from distributing funds is often lower than the Vorabpauschale (pre-tax levy) on accumulating ones. When you eventually need the money for retirement, switch strategies.

And if you’re also trading derivatives in Austria, note that the special taxation rules for derivatives can interact with your ETF portfolio in unexpected ways, worth knowing before you start experimenting with options.

The Bottom Line

The Vorabpauschale (pre-tax levy) is Austria’s way of saying “we want our cut now, not later.” It’s frustrating, it’s mathematically weird, and it reduces your compounding power.

But understanding it is part of the price of investing in Austria. A 0.2% annual tax drag on your portfolio isn’t the end of the world, but it’s enough to make you think twice about which ETF you choose, and whether distributing funds might actually be smarter for your specific situation.

The real trick? Run the numbers. Use the tools available. And never, ever assume that two ETFs with identical holdings have the same tax burden. In Austria, they absolutely do not.